Hard Red Winter Wheat is one of the grain commodities, along with soft red wheat, corn, soybeans and others. Within the wheat family, first of all, there is a fundamental difference between two wheat types. Soft wheat is low in protein and is basically used in cakes in pastries. By contrast, hard wheat has a higher content of protein and it founds itself in breads and hard baked goods. Some time ago, trading of hard wheat took place at Kansas City Board of Trade. Then, it moved to Chicago. One can trade hard wheat futures at Chicago Board of Trade under the ticker $KE. Hereby, the contract size is 5’000 bushels (300’000 pounds) each and the prices are in Dollars US per 100 bushel.

In the last article from September 2022, we saw prices climbed from 524 USD in December 2020 towards 738 USD by August 2021. There, we have forecasted a rally towards 1’000 USD and higher to take place. We were right. In May 2022, hard red winter wheat has printed a highest price since a good decade at 1225. Now, we expect a short term pullback. Then, a rally towards 1’500 USD and higher should take place.

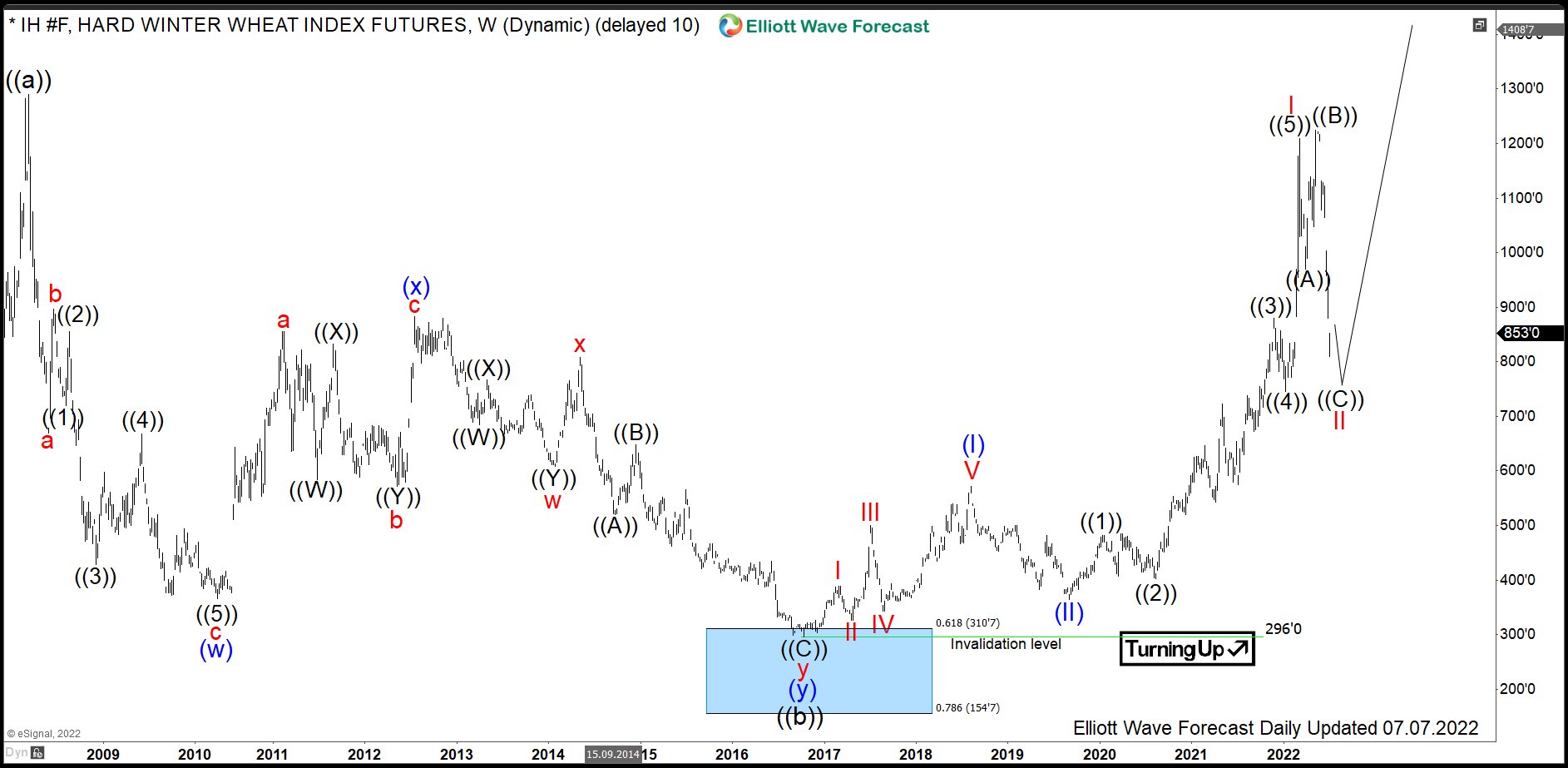

Hard Red Winter Wheat Weekly Elliott Wave Analysis 07.10.2022

The weekly chart below shows the Hard Winter Wheat front contract IH #F. From the all-time lows, the prices have developed a cycle higher in black wave ((a)) of a grand super cycle degree. It has ended in March 2008 at 1290 Dollars. From the highs, a correction lower in wave ((b)) has unfolded as an Elliott Wave double three pattern. In 8 years, as a matter of fact, IH #F has lost more than 3/4 of the price reaching 296 Dollars per 100 bushel. It is the preferred view that an important bottom on October 2016 has been set and the black wave ((b)) has ended.

From the lows, consequently, a new rally within wave ((c)) may have started. Hereby, the super cycle degree waves (I) and (II) have already ended, while above 365, wave (III) is extending higher. It has hit 1225 and, therefore, reached beyond the 2.618 extension of the wave (I) being 1094 USD. As a consequence, wave (III) might have ended. However, the RSI reading still shows a divergence as related to the wave (I). Therefore, acceleration within red wave III of blue wave (III) should still take place.

The preferred view is that wave I has ended in March 2022 at 1209 USD. From the highs, the correction in wave II is unfolding as an expanded flat structure. Then, acceleration in wave III of (III) should take place. The medium-term target for coming 1-2 years will be towards 1’500 USD per 100 bushel and even higher. Investors and traders can be looking to buy the pullback in wave II against 365 lows expecting more upside.

2023-2025, the expectations are to break out to the new all-time highs. The long-term target for wave ((c)) to end will be 1444-2153 area.

Source: https://elliottwave-forecast.com/commodities/hard-red-winter-wheat-shortage-2023/